Swiss Derivative Award 2026

Dr. Anian Roppel was awarded with the 2nd place at the Swiss Derivative Awards 2026 in Zurich for his working paper with Nils Unger und Marliese Uhrig-Homburg "Option-implied lower bound beliefs and the impact of negative interest rates". The working paper is part of his dissertation "Macro-Finance, Asset-Pricing and the Role of Investor Beliefs".

Science Award 2024 of the KIT-Department of Economics and Management

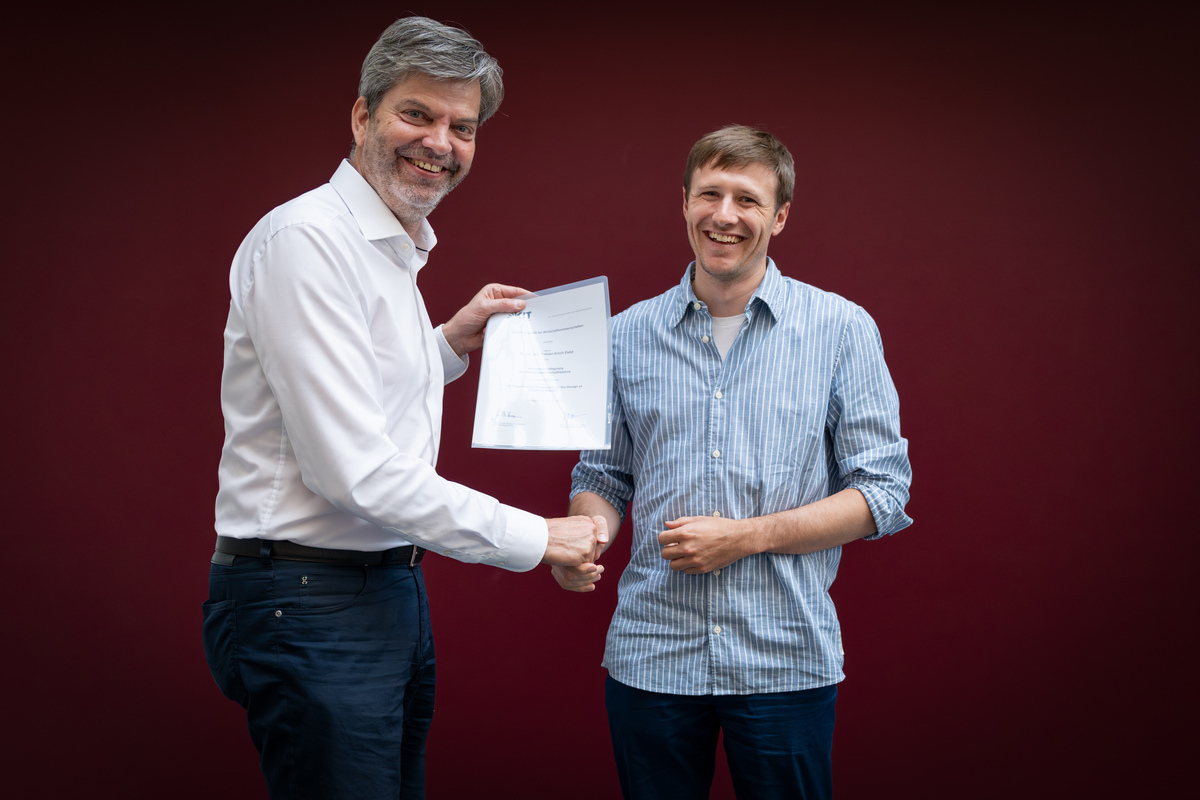

As part of this year's Dialogue Day on June 26, 2025, the dissertation "An Asset Pricing Perspective on the Design of Cryptocurrencies" by Dr. Fabian Eska was awarded the Science Prize of the KIT-Department of Economics and Management in the category Business Administration. The dissertation examines how specific design features - such as the consensus mechanism, the reward system or the degree of anonymity - influence the value, volatility and risk of cryptocurrencies. The work combines classical financial market theory with modern crypto technology and provides valuable insights for investors, developers and regulators. Here you find the explanation video.

Science Award 2021 of the KIT-Department of Economics and Management

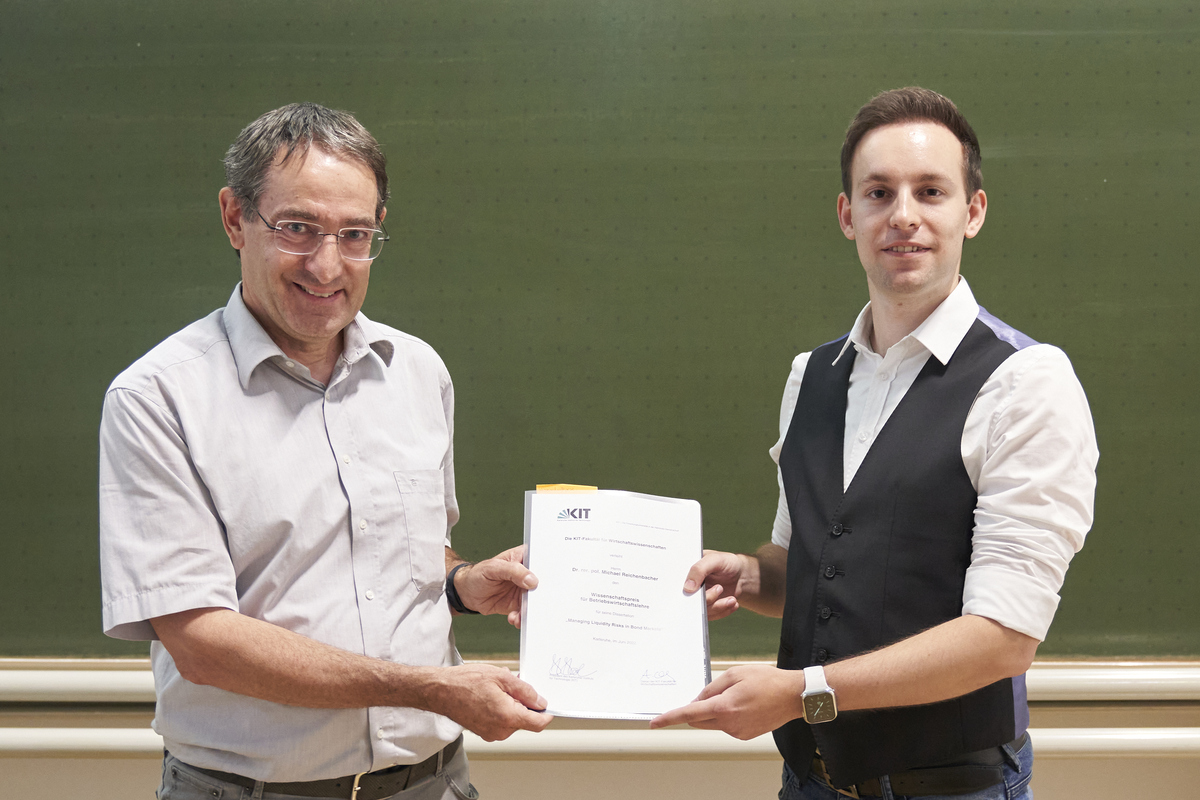

In the course of this year's annual faculty celebration on June 23, 2022, the dissertation "Managing Liquidity Risks in Bond Markets" by Dr. Michael Reichenbacher was awarded the Science Award of the KIT-Department of Economics and Management in the category of Business Administration. The dissertation deals with with the management of liquidity risks in bond markets. It aims to contribute to the quantification of liquidity risks and proposes own approaches for a precise measurement and prediction of liquidity as well as statistical tests for the evaluation of predictive models.

Science Award 2020 of the KIT-Department of Economics and Management

On June 24, 2021, the dissertation "Asset Pricing Bricks" by Dr. Marcel Müller was awarded the Science Award of the KIT-Department of Economics and Management in the category Business Administration. In his dissertation, Dr. Müller investigates the influence of different sources of risk on the prices of securities. For this purpose, he uses, among other things, machine learning methods that draw on innovative data sets. Dr. Müller summarized the content of his work in a short video for the award ceremony during the virtual event (in German):

Science Award 2019 of the KIT-Department of Economics and Management

At this year's faculty anniversary celebration the dissertation "Frictions, Intermediaries, and the Option Market" by Dr. Michael Hofmann was awarded the Science Award 2019 of the KIT-Department of Economics and Management in the category Business Administration. Dr. Hofmann summarized the content of his thesis in a short video for the award ceremony during the virtual event:

Swiss Derivative Awards 2020

At the Swiss Derivative Awards 2020, Dr. Michael Hofmann's dissertation "Frictions, Intermediaries, and the Option Market" was awarded a shared second place in the Research Awards section. Further information on the Swiss Derivative Awards and the prize winners can be found on the Swiss Derivate Awards homepage.

Swiss Derivatives Awards 2019

The dissertation "Hedging Frictions and Option Values" by Dr. Stefan Kanne was awarded second place at the Swiss Derivatives Awards 2019. The Research Award is given to the best scientific papers dealing with derivatives and structured products. It is sponsored by the Swiss Structured Products Association (SSPA).

Science Award 2017 of the KIT Faculty of Economics

Dr. Martin Hain was awarded the Science Prize for Business Administration of the KIT Faculty of Economics for his dissertation "Understanding Energy Commodity Price Risks".

Honorary Evening of the President 2017

On July 12, 2017, Dr. Philipp Schuster was honored by the President for his award of the FIRM Research Prize 2016 for his dissertation "Liquidity in Bond Markets" together with other KIT prize winners.

Walter-Georg-Waffenschmidt Prize for Business Administration

The KIT Faculty of Economics awarded Dr. Schuster the Science Prize for Business Administration 2016 for his dissertation "Liquidity in Bond Markets".

FIRM Research Prize 2016

Under the patronage of the Hessian Minister of Economics, Energy, Transport and Regional Development, Tarek Al Wazir, the Frankfurt Institute for Risk Management and Regulation (FIRM) awarded the Research Prize 2016 to Dr. Philipp Schuster on 30.06.2016.

Dr. Philipp Schuster was able to assert himself with his dissertation "Liquidity in Bond Markets", in which he analyzed the liquidity of bond markets. "The thesis compares the quality of different liquidity measures in a very convincing way. It uses a cleanly constructed model framework to analyse the influence of maturity, transaction costs and investor behaviour on trading volumes and bond prices," said jury chairman Günter Franke, retired Professor of International Financial Management at the University of Constance and Co-Chairman of the Advisory Board of FIRM.

For further information please click here.

University Prize of the Deutsches Aktieninstitut 2015

Dr. Philipp Schuster received the University Prize of the Deutsches Aktieninstitut (DAI) in the category "Dissertations". The university prize, which is endowed with a total of 20,000 euros, is awarded annually for the best academic dissertations on the topic of "Stocks and Capital Markets".

The prize was awarded for the habilitation thesis of Prof. Dr. Thilo Kuntz, who dealt with the topic "Structuring of corporations between freedom and compulsion - venture capital in Germany and the USA". The university prize for dissertations (prize money 10,000 euros) was shared by Dr. Denefa Bostandzic with her thesis on "Systemic Risk and the Financial System" and Dr. Philipp Schuster, who wrote his doctoral thesis on "Liquidity in Bond Markets". According to the jury, both works convinced with their above-average scientific achievements.

KIT Doctoral Prize 2015

With his dissertation "Carbon Finance: Equilibrium Modeling and Empirical Analysis", Dr. Hitzemann won the KIT Doctoral Prize 2015, which promotes outstanding achievements of young scientists at KIT.

Energy & Finance Conference Best Paper Award 2013

Prof. Uhrig-Homburg and Mr. Hitzemann received the Best Paper Award 2013 for their research on Empirical Performance of Reduced-Form Models for Emission Permit Prices at the Energy & Finance Conference.

Walter-Georg-Waffenschmidt Prize for Business Administration 2011

The Faculty of Economics and Management awards the 2011 Science Prize for outstanding scientific work to the dissertation of Dr. Michael Triskatis on the topic "CO2 emission certificates - price modelling and derivatives valuation".

DGF Best Paper Award 2011

Prof. Uhrig-Homburg and Mr. Hitzemann will be awarded the Best Paper Award 2011 at the conference of the German Society of Finance with their research work on price modeling in the CO2 market.

1st place at the Postbank Finance Award 2008/2009

The first prize of this year's Postbank Finance Award went to the University of Karlsruhe (TH). The team around Prof. Dr. Marliese Uhrig-Homburg, consisting of Jasmin Berdel, Daniel Müller and Florian Stegmüller, examined - based on the credit crisis - the weaknesses of common risk assessment procedures for the securitization of loan portfolios. The group developed concrete proposals on how such risks can be better identified and presented more transparently and - above all - how they can be contained. To this end, a portion of the risk should remain with the originator of the securitization.

38 teams (students and their university professors) from Germany and Austria took part in the 6th Postbank Finance Award, Germany's highest-endowed Banking & Finance university competition. The submitted works present scientifically sound answers to the "lessons of the financial crisis", provide impulses and stimulate the discussion on this important topic. A jury of experts from business, science and media evaluated the entries.

2nd place at the Postbank Finance Award 2006/2007

Under the direction of Prof. Marliese Uhrig-Homburg, students from the University of Karlsruhe (TH) Marwan El Chamaa, Stefan Helber, Daniel Herzig, Jonathan Nickels Küll and Johannes Rudek achieved a remarkable second place in the Postbank Finance Award. They developed a new certification concept for external ratings.